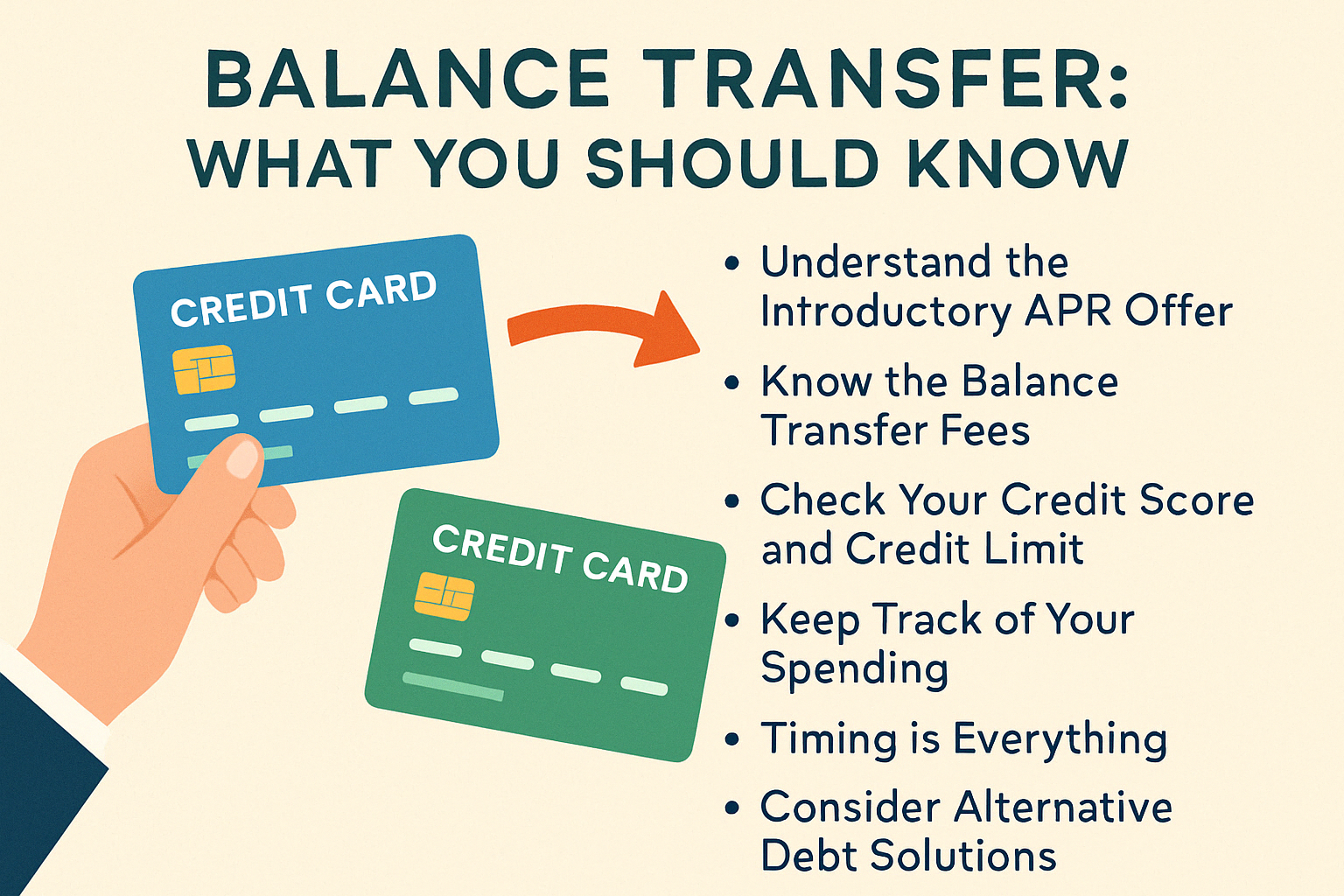

Things to Consider Before Making a Balance Transfer

If you’re struggling with credit card debt, you might have heard of a balance transfer as a way to make your payments more manageable. At its core, a balance transfer allows you to move debt from one credit card to another, often with a lower interest rate. It sounds like a great deal, especially if you’re paying high interest on your current card. But before you rush into transferring your balance, there are a few things you should know. Depending on your financial situation, it could be a smart way to manage your debt, but there are details that could catch you off guard. In fact, if you’re someone with less-than-perfect credit, you might also consider debt consolidation loans with bad credit to help get your finances under control.

Here’s a guide to help you weigh the pros and cons and understand exactly what you’re signing up for before making that balance transfer.

Understand the Introductory APR Offer

Many credit cards offer an introductory 0% APR for balance transfers for a certain period, typically between 6 to 18 months. This sounds appealing, but it’s important to read the fine print. The 0% interest rate only lasts for the introductory period, and after that, your interest rate may jump significantly-sometimes to as high as 20% or more.

What does this mean for you? If you’re planning to transfer a balance, you need to make sure you’ll be able to pay it off before the introductory period ends. If you don’t, you could end up paying high interest on the remaining balance, which could negate the benefits of the transfer.

Know the Balance Transfer Fees

Even if the APR is low or 0%, there’s a good chance you’ll have to pay a balance transfer fee. These fees typically range from 3% to 5% of the amount you transfer. For example, if you transfer $5,000 to a new card with a 5% fee, you’ll be charged $250 just for making the transfer.

While this fee is often seen as a cost of doing business for credit card companies, it’s important to factor this into your decision. Sometimes, even a lower interest rate won’t save you money if the balance transfer fee is too high. Be sure to calculate whether the interest savings outweigh the fee.

Check Your Credit Score and Credit Limit

Before you even consider transferring a balance, take a look at your credit score. If your score is lower than you’d like, you might not qualify for the best balance transfer offers. Cards with the best 0% APR offers often require good to excellent credit, so if your score isn’t up to par, you might want to explore debt consolidation loans with bad credit. These loans could provide a way to consolidate multiple debts into one monthly payment, with a potentially lower interest rate than your current credit card rates.

Additionally, ensure the credit limit on the new card is high enough to cover your transferred balance. If it’s not, you may need to transfer only part of your debt, or you could be left with an incomplete solution. Transferring less than the full balance may not make a significant difference in your finances.

Keep Track of Your Spending

A balance transfer can be a great tool to pay off debt, but it’s essential to understand that it’s not a solution to your spending habits. The whole point of transferring a balance is to save money on interest and pay down your debt faster, but if you continue using your old credit card or rack up new charges on your balance transfer card, you could find yourself in even deeper debt.

Some people make the mistake of treating the balance transfer as a fresh start, only to keep charging their cards to the max. If you’re not careful, you’ll find yourself with more debt than you originally had, and the transfer won’t help you at all in the long run.

Timing Is Everything

When you transfer a balance, timing is key. Be aware of the date your introductory APR ends and make sure you’ve made a plan to pay off your balance before that period expires. The closer you get to the end of the 0% APR period, the more interest you’ll start paying. If you’re not careful, the interest could quickly outpace any savings you gained from the transfer.

For example, let’s say you’ve transferred $3,000 to a new card with 0% APR for 12 months. If you don’t pay it off by the end of the year, the remaining balance will be hit with a much higher APR, and you’ll be back to paying high interest rates. This is why it’s so important to have a solid plan in place for paying off your balance before the introductory period expires.

Understand the Impact on Your Credit Score

While balance transfers can be useful, they can also affect your credit score-both positively and negatively. When you open a new credit card for the transfer, your credit score could dip slightly due to the hard inquiry that comes with applying for a new card. However, if you manage the new card responsibly, it could eventually help your credit score by lowering your overall credit utilization the ratio of credit you’ve used versus your credit limit.

On the flip side, if you continue carrying a balance on the new card or miss payments, your credit score could take a hit. It’s important to be aware of how your credit will be impacted and make sure that transferring the balance is actually going to help, not hurt, your credit in the long term.

Consider Alternative Debt Solutions

Balance transfers can be a helpful tool, but they aren’t always the best solution for everyone. If you’ve been struggling with debt for a while, you may want to look into other options for managing your debt, such as debt consolidation loans with bad credit or working with a financial advisor to create a personalized repayment plan. Consolidation loans could help simplify your payments and potentially lower your interest rate, especially if you have multiple high-interest debts.

Debt consolidation can help you manage payments on multiple debts with one fixed interest rate, and it might be more effective if you’re not confident about paying off a balance transfer within the 0% APR period.

Final Thoughts: Weighing the Pros and Cons

Before jumping into a balance transfer, take the time to carefully consider all aspects of the offer and how it fits with your financial situation. A balance transfer can help you save money on interest and pay off your debt faster, but only if you use it wisely. Be mindful of fees, interest rates, and your overall financial habits. If you’re not confident that a balance transfer is right for you, consider other options, like debt consolidation loans or speaking with a financial advisor to get personalized advice.

In the end, the most important thing is to make a plan that works for you and stick to it. A balance transfer could be a smart move, but only if it’s part of a larger strategy to get your debt under control and start building better financial habits.